1 Clear Signal That Nvidia's Stock Is Primed to Skyrocket | The Motley Fool

Nvidia (NVDA 1.58%) has made investors a ton of money over the past few years. If you invested $10,000 into it at the start of 2023, that investment is now worth $125,000. That’s an incredible return on investment. While Nvidia won’t be able to repeat that growth rate over the next three years, it has what it takes to outperform the market.

I think there’s one clear signal investors can’t ignore about Nvidia’s stock, and they should heed it and scoop up shares before the rest of the market catches on.

Image source: Nvidia.

The market only expects one more year of strong growth

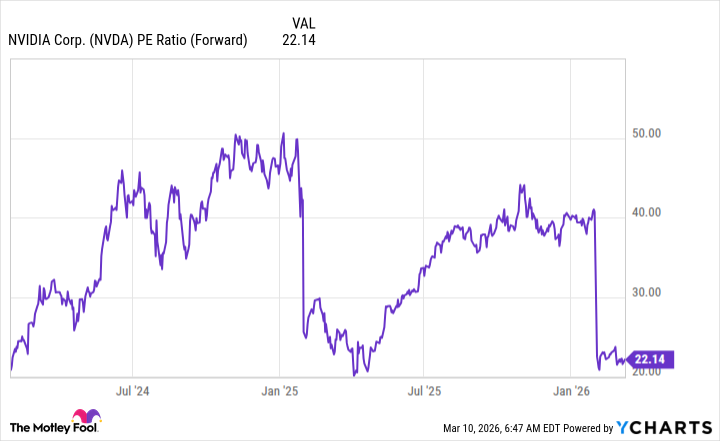

Nvidia’s stock has somehow gotten the stigma that it’s expensive, but that couldn’t be further from the case. Right now, it trades at 22.1 times forward earnings, nearly the same price-to-earnings ratio as the S&P 500which trades at 21.7 times forward earnings.

NVDA PE Ratio (Forward) data by YCharts

Normally, market-average premiums are reserved for stocks growing at a market-average pace, but that’s not Nvidia. In its last quarter, it grew revenue by 73%. For this quarter, management expects 77% growth. Normally, the market grows at about a 10% pace each year, so this is a massive mismatch.

The current price tag on Nvidia’s stock assumes that it will have a strong year, but will revert to market-average growth in 2027. But I don’t think that’s true.

Nvidia projects that global data center capital expenditures will reach $3 trillion to $4 trillion by 2030. McKinsey & Company offered a similar projection, estimating that it will take $7 trillion in cumulative spend by 2030 to meet demand for artificial intelligence (AI). That clearly indicates growth for Nvidia will last for multiple years past 2026, crushing the bear case on the stock.

Today’s Change

(-1.58%) $-2.89

Current Price

$180.25

Key Data Points

Market Cap

$4.4T

Day’s Range

$179.94 – $186.09

52wk Range

$86.62 – $212.19

Volume

161M

Avg Vol

175M

Gross Margin

71.07%

Dividend Yield

0.02%

One common misconception out there is that Nvidia cannot grow because AI hyperscalers are maxing out their cash flows devoted to capital expenditures. While that is partly true, investors are forgetting that much of the capital expenditure right now is going toward constructing data centers. It takes years for data centers to come online once announced, and computing units are the last thing to be purchased.

So, while capital expenditure growth may not be as easy to come by, the proportion of that spending devoted to computing units will increase dramatically. Other regions of the world (namely, Europe) haven’t even started on AI infrastructure, so this could be another source of growth.

This bodes well for Nvidia’s futureand investors should use this low price as their opportunity to load up before the market realizes it will deliver strong growth again in 2027 and beyond.